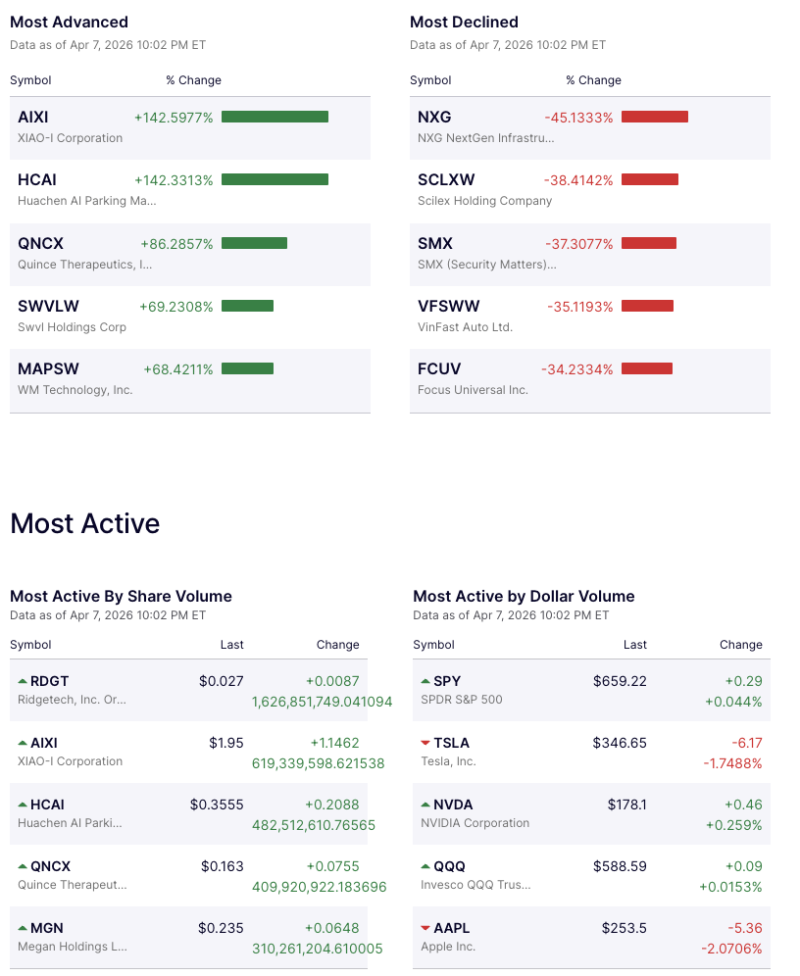

US markets closed with a stark split between speculative microcap euphoria and measured institutional positioning in mega caps, underscoring a two-layer tape dominated by liquidity extremes. On the speculative side, XIAO-I Corporation (AIXI) soared 142.60% to $1.95, while Huachen AI Parking Management (HCAI) jumped 142.33% to $0.3555, making them the day’s most advanced stocks. Momentum extended into biotech and tech-adjacent names, with Quince Therapeutics (QNCX) up 86.29%, SWVL Holdings (SWVLW) gaining 69.23%, and WM Technology (MAPSW) rising 68.42%, pointing to aggressive breakout chasing in low-float names.

The flip side was equally violent. NXG NextGen Infrastructure (NXG) plunged 45.13%, Scilex Holding warrants (SCLXW) fell 38.41%, and SMX (Security Matters) dropped 37.31%, while VinFast Auto warrants (VFSWW) lost 35.12% and Focus Universal (FCUV) declined 34.23%. The sharp reversals in names that had recently featured among top gainers suggest the session was marked by rapid momentum unwinds, profit booking, and fragile sponsorship in speculative counters.

Liquidity data showed where the real institutional money sat. By share volume, Ridgetech (RDGT) led with over 1.62 billion shares traded, followed by AIXI (619.3 million), HCAI (482.5 million), and QNCX (409.9 million), confirming that retail-driven flows remained concentrated in sub-$2 names. But by dollar volume, the leadership shifted decisively to core market proxies and mega caps: SPDR S&P 500 ETF (SPY) topped the list at $659.22, up 0.04%, followed by Tesla (TSLA) at $346.65, down 1.75%, NVIDIA (NVDA) at $178.10, up 0.26%, Invesco QQQ Trust (QQQ) at $588.59, and Apple (AAPL) at $253.50, down 2.07%.

The session’s combined tape reinforces a barbell market structure: speculative capital is crowding into AI- and biotech-linked penny stocks with explosive percentage moves, while institutional liquidity remains anchored in SPY, Tesla, Nvidia, QQQ, and Apple. The divergence between 142% surges in AIXI and HCAI versus weakness in Tesla and Apple suggests that while headline risk appetite remains elevated, serious capital is still favoring liquid index vehicles and proven AI infrastructure leaders over broad-based equity beta.