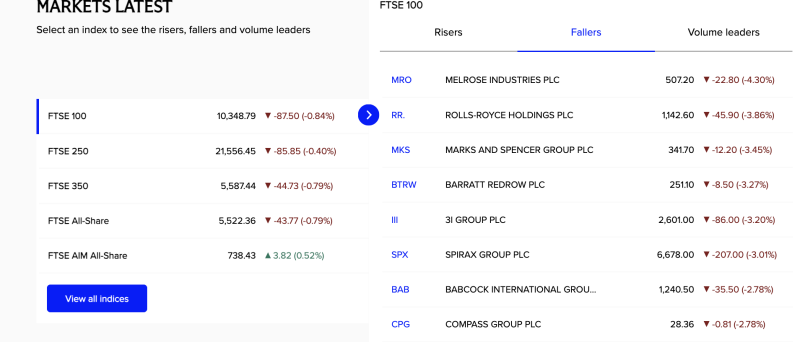

Global markets moved into a more defensive posture as UK equities joined the selective risk rotation already visible across Wall Street and crypto, deepening the divide between quality leadership and cyclical profit-taking. The FTSE 100 fell 0.84% to 10,348.79, while the FTSE 250 lost 0.40%, FTSE 350 slipped 0.79%, and the FTSE All-Share declined 0.79%, signaling broad-based weakness across large and mid-cap UK stocks. The only bright spot came from the FTSE AIM All-Share, up 0.52%, indicating speculative flows remain active in smaller growth names even as benchmark indices softened.

The heaviest pressure in London came from industrials, aerospace, consumer names, and capital goods. Melrose Industries (MRO) dropped 4.30% to 507.20, Rolls-Royce Holdings (RR.) fell 3.86% to 1,142.60, and Marks & Spencer (MKS) declined 3.45% to 341.70, suggesting investors were locking in gains in cyclical leaders that had previously outperformed. Housing and industrial engineering names also weakened, with Barratt Redrow (BTRW) down 3.27%, 3i Group (III) off 3.20%, and Spirax Group (SPX) losing 3.01%, reinforcing a wider valuation reset in economically sensitive sectors. Additional downside in Babcock International (BAB) and Compass Group (CPG), both down 2.78%, highlighted the breadth of the pullback.

The weakness in UK cyclicals contrasted with continued resilience in US mega-cap technology and crypto majors. Apple (AAPL), Amazon (AMZN), AMD, Micron (MU), and NVIDIA (NVDA) remained supported by AI infrastructure and earnings visibility, while Bitcoin (BTC) held near $68,767 and Ethereum stayed above $2,100, signaling that institutional liquidity continues to favor global quality growth and digital large caps. At the same time, violent moves in microcaps, altcoins, and UK small caps show speculative risk appetite has not disappeared—it has simply narrowed into lower-float, narrative-driven trades.